How is El Nino Impacting The South East

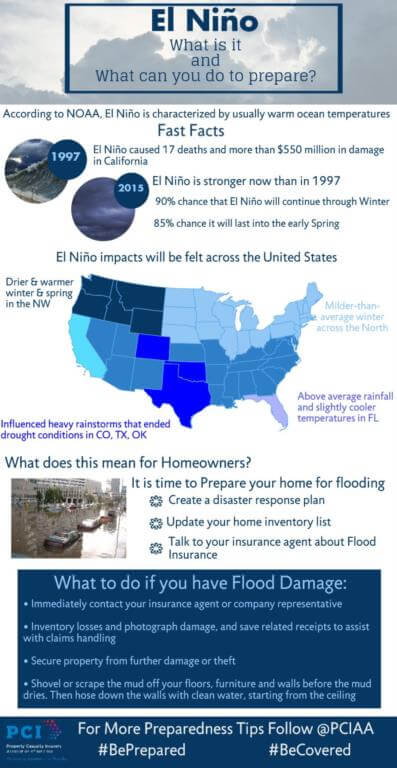

El Nino actually isn’t all that bad like most of us think. The global impacting climate cycle know as El Nino will bring a cooler, wetter climate to our area helping to reduce hurricane activity in the Atlantic and wildfires.

El Nino actually isn’t all that bad like most of us think. The global impacting climate cycle know as El Nino will bring a cooler, wetter climate to our area helping to reduce hurricane activity in the Atlantic and wildfires.

However, there will be increased chances for severe storms throughout the winter along with greater chances of flooding.

Homeowners and Businessowners Insurance does NOT cover flooding! There is a 30-day waiting period before flood insurance goes into affect, so don’t wait.

With an increased chance of flooding this spring now is the time to either add a flood policy or update an existing policy. Even just 2 inches of water can cause in excess of $20,000 in flood damages!

If you have questions about flood insurance we can help 850.770.7047